Insurance can be profitable. Are you retaining the profitability of your policies?

GROUP CAPTIVES

“There’s just something about having a high level of control over your insurance destiny… this is exactly what our group captive has done to LionHeart.”

What is captive insurance?Group captive insurance is the most efficient risk financing mechanism available to qualifying middle-market businesses.

Yet most business owners have never heard of it. Polarix specializes in helping companies join, structure, and maximize group captive programs that turn insurance premiums from a cost into a long-term asset.

CASE STUDY

See how LionHeart built $400,000 in equity on a $1.4M insurance spend over a five-year period after joining a group captive.

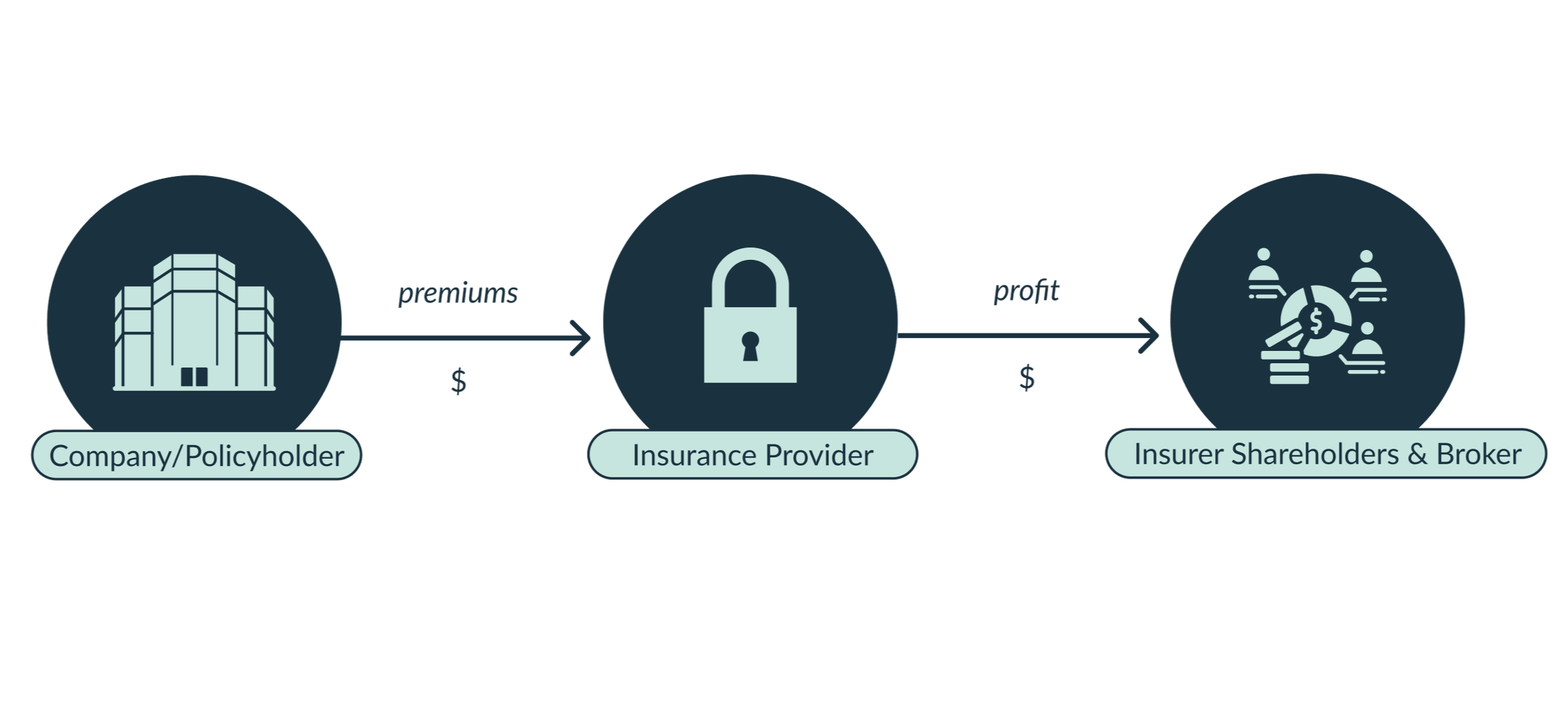

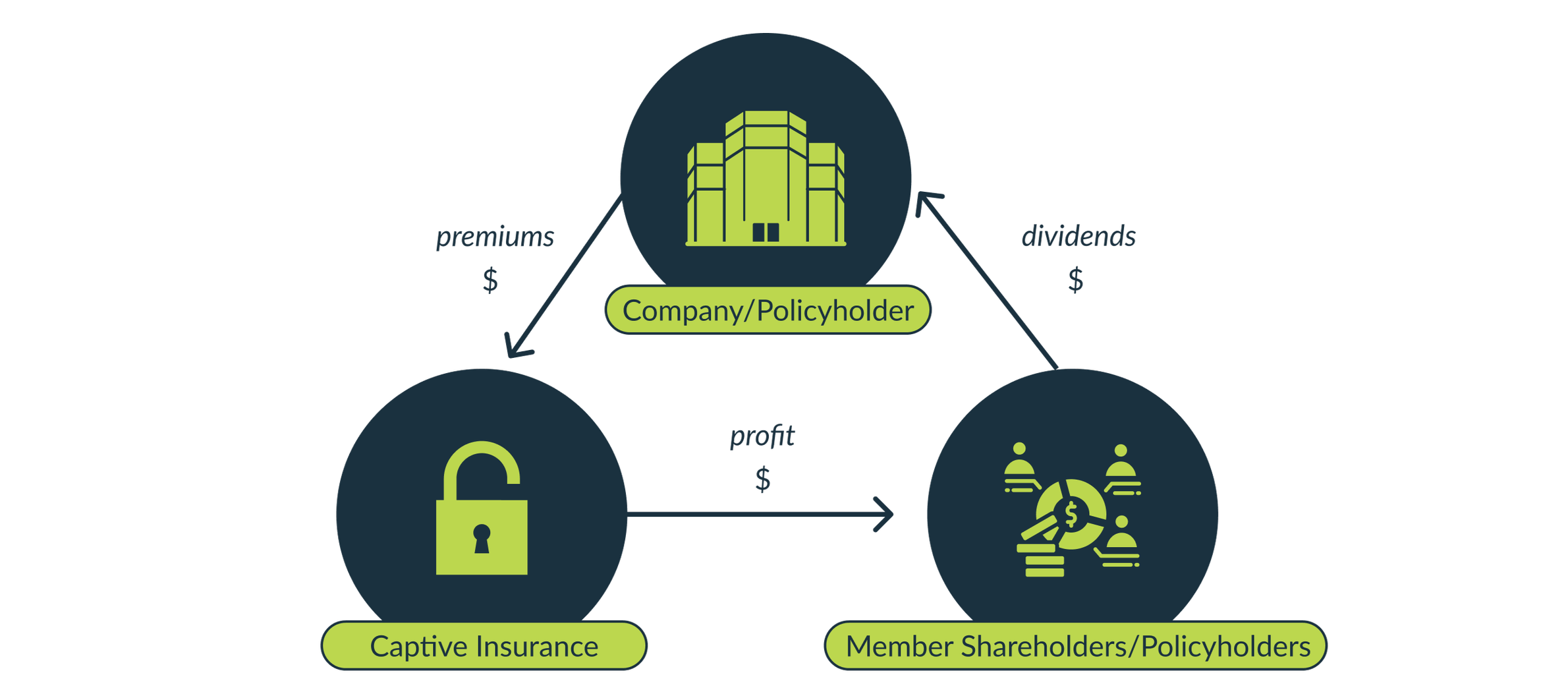

Traditional Insurance vs. Captive Insurance

-

Traditional Insurance

In traditional retail insurance, you pay premiums and the carrier retains the underwriting profit. When you have a good year (i.e., no claims, no incidents), that money is gone. You've essentially funded someone else's profit margin.

-

Captive Insurance

A group captive is different. You and a group of like-minded, well-run businesses pool together to form your own insurance company. You maintain coverage, but you also own a stake in the captive, which means underwriting profits, investment income, and favorable loss experience come back to you.

The result? Insurance becomes an investment.

Captive members don’t just save on premiums. They build equity. They gain control over their program design, claims management, and risk culture. Over time, a well-run captive program can generate returns that rival other capital investments in your business.

Take the first step towards insurance equity — let us model your potential returns.

The path to captive membership

-

1

Polarix evaluates your claims history, safety record, and premium profile to determine eligibility.

-

2

We model the potential equity and savings you could have retained over the prior 5 years.

-

3

If it's a fit, we guide you through the membership process and onboard you to the right group.

-

4

We manage ongoing reporting, loss control, and strategic advisory to maximize your program performance.

Captives aren’t for everyone, but they could be for you.

-

Qualifying businesses typically share a few traits: They operate in physical industries (construction, manufacturing, equipment, transportation), they have a strong safety culture and low claims frequency, and they spend $150,000 or more in aggregate annual premium for Workers Compensation, General Liability, and Auto. If that sounds like your business, you may be leaving significant money on the table.

-

Over time, captive members see:

Underwriting profits returned to member-owners

Investment income on reserves

Greater control over claims management and vendor selection

Long-term equity built inside the captive structure

Improved safety culture and risk management practices

-

Contact us to determine your company’s eligibility.

Why switch from retail insurance to a group captive?

While each of our clients has a different reason for making the switch, there are a few common drivers.

-

![]()

Profitability

Captives enable companies to retain underwriting profits and investment income that would otherwise go to external insurers. This means higher profitability and a more assured financial future for the business and its owner.

-

![]()

Risk Management

Joining a captive can also lead to improved risk management strategies and better alignment of insurance with overall business goals.

-

![]()

Decision-Making Ability

As a member-owner, you play an active role in the decision-making of the group, gaining an unrivaled level of transparency and control over your insurance.

-

![]()

Owner Network

By being part of a group with other high-performing companies, you have the opportunity to connect with fellow top operators, fostering a network of excellence.

-

![]()

Aligned Incentives

Captive Groups align the incentives of both policy holders and brokers and ensure everyone is working toward lower costs and higher-performing organizations.

Not yet eligible for a group captive?

Polarix partners with leading risk management experts to help companies reduce risk and become eligible for captive insurance programs. Contact us to learn how Polarix and our network of partners can help you gain eligibility.

Find out what your insurance program could be worth.

Our team will run a complimentary analysis of your current program and model what captive membership could look like for your business, including a projection of equity you could have retained over the past five years.